State of the Industry Survey

2009 is a year a lot of people are happy to have in their rear-view mirror. As the year drew to a close, some economists pointed to hopeful signs of a nascent recovery, while others expressed disappointment that the economy didn’t rev up more in the fourth quarter of 2009.

With a lot of question marks about the overall economy and the construction industry going into 2010, we wanted to see how roofing contractors felt the economic environment would impact their businesses.

Architectural Roofing & Waterproofing and Roofing Contractor magazines and BNP Media Market Research conducted a research study to gauge roofing contractors’ sense of the commercial and residential roofing markets. We wanted to see how contractors fared in 2009 and how they expected their businesses to perform in 2010 and over the next three years. The research study was conducted from Nov. 10 though Dec. 31, 2009. BNP Market Research contacted 15,529 roofing contractors for the Web-based study, and 297 respondents completed surveys online for a response rate of 2 percent.

• Measuring sales volumes in 2009, 2010, and over the next three years.

• Determining trends among different product categories.

• Evaluating current and expected inventory levels and manufacturer relationships.

• Assessing the business conditions and employment levels in the roofing industry.

• Indentifying key problems contractors currently face.

An overview of the results shows that while 2009 was more difficult than expected, contractors are generally optimistic about their performance in 2010 and over the next three years.

An overwhelming majority of participants were high-ranking members of their companies; 79 percent of respondents listed their title as owner, president, vice president or CEO, while another 18 percent were managers or supervisors. The companies they work for were pretty evenly spread across the country, with 27 percent from the South, 26 percent from the West, 25 percent from the Midwest and 22 percent from the Northeast.

They represented companies of all different sizes. While the companies in the survey averaged 55 employees, half of the respondents employed 10 people or less. More than a quarter employed four or less.

Gross annual sales for these companies averaged $4,773,225 in 2009, down from $4,994,939 in last year’s survey. Nearly three-fifths (58 percent) reported annual sales of at least $1 million in 2009.

The companies perform a mix of residential and commercial work. About one-fifth of study participants exclusively do residential work, while another fifth only do commercial work. The remaining 60 percent do some combination of both residential and commercial work.

Figure 1 lists the percentage of roofing contractors involved in each sector of the market. Seventy-seven percent of respondents do at least some residential replacement work, 69 percent do residential repairs, 66 percent do commercial replacement, and 67 percent do commercial repairs. About half of respondents do some residential new construction (48 percent) and commercial new construction (49 percent).

The chart in Figure 2 shows the amount of revenue contractors derive from each of these market segments. On average, 38 percent total revenue comes from residential replacement and 23 percent from commercial replacement. Thus 61 percent of total revenue comes from some form of replacement, and another 18 percent comes from commercial and residential repairs. Commercial new construction accounts for 13 percent of revenues, while residential new construction accounts for 8 percent.

Our survey results confirm that for many 2009 was a tough year, as more than half of the contractors surveyed had annual sales come in below 2008 totals. However, they expect better results in 2010 and beyond.

As Figure 3 shows, 53 percent of respondents saw sales drop in 2009, while 27 percent saw an increase. Twenty percent had sales stay bout the same. The results from 2009 are worse than those of 2008, in which 39 percent experienced lower sales than the previous year and 45 percent saw increases. Last year was also worse than predicted. In last year’s survey, 30 percent expected a decrease in sales in 2009, while 53 percent actually saw a decline; 49 percent expected sales to increase in 2009, and only 27 percent posted increases.

Most are optimistic that sales volume will increase in 2010 and over the next three years. More than half of participants expect sales to increase this year, while 24 percent expect them to decrease and 25 percent expect them to stay the same (Figure 4). The long-term outlook is even better, with more than three-quarters of contractors surveyed expecting sales volumes to increase over the next three years (Figure 5).

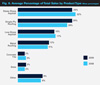

As Figure 6 shows, steep-slope asphalt and single-ply roofing products accounted for the biggest share of contractors’ business last year. On average, 29 percent of revenue came from steep-slope asphalt products and another 29 percent came from single ply. These were also the top two categories in last year’s survey, which had steep-slope asphalt at 32 percent and single ply at 26. The 3 percent drop in steep-slope asphalt coinciding with the 3 percent rise in single ply brought the two into a tie for the top spot in 2009. The survey shows more contractors are installing single-ply systems; 68 percent installed them in 2008 compared to 73 percent in 2009.

Breaking down 2009 sales by product category, almost every segment saw a double-digit differential between those seeing a decrease and those seeing an increase in sales (Figure 7). Far more contractors saw a decrease than saw an increase in all product categories except single ply and metal roofing. Metal was the only category to have more contractors experience increases rather than decreases in sales. In fact, metal was the only product in positive territory, with a net differential of plus 6 percentage points. Single ply was the category with the next best performance (a differential of minus 4 percentage points).

The steepest declines were seen in low-slope asphalt (minus 26 percentage points) and concrete tile (minus 33 percentage points).

Questions centering on business conditions, prices and employment levels seem to confirm that 2009 was a tough year. Two-thirds of respondents thought business conditions were worse in 2009 than they were in 2008. However, only 30 percent expect them to decline this year, while 33 percent expect them to stay the same and 36 percent expect them to improve.

Contractors seem resigned to price increases, with more than three-quarters of participants reporting the cost of doing business rose in the past year. Three-quarters of contractors expect costs to continue to rise in 2010.

The survey shows employment levels dropped again in 2009, with 64 percent reporting the number of employees in the roofing industry declined from the previous year’s level. About two-thirds predict employment levels will stay the same or increase in 2010, while 35 percent expect employment numbers to drop.

Asked to identify the biggest challenges facing roofing contractors in the year ahead, participants listed a variety of concerns. The most common responses focused on increased material costs and lowball bids and pricing wars inspired by increased competition. Insurance/health care costs were the third most common concern mentioned, followed by simply finding enough work and the poor overall economy. Despite the slowdown in construction, contractors listed finding qualified employees as the sixth most common challenge, followed by government regulation/intervention.

FMI’s Construction Forecast

Heather Jones, Construction Economist for FMI Corporation, shared some of the data from FMI’s most recent construction forecast. “The outlook for put in place construction for 2010 remains bleak,” she said. “Total construction in 2010 will be down 4 percent after declining 13 percent in 2009. While 2009 was likely the bottom in terms of percent decline, 2010 will be the bottom in terms of dollar volume. Residential construction is expected to begin recovering in 2010. Nonresidential construction will decline 15 percent in 2010 after declining 10 percent in 2009. Non-building construction will continue to be a positive contributor, increasing another 5 percent in 2010, driven mostly by conservation and development construction. The residential sector is expected to begin to recover in 2010. Single-family put in place construction will recover at a slower rate than single family housing starts. The number of square feet per start is declining, meaning that new homes are getting smaller. They are also getting less expensive. The average and median new home sale price is decreasing. The first time home buyer credit and recessionary environment were contributing factors to this decrease. Multi-family construction has been impacted severely by tight credit and will not recover until credit loosens. Residential improvements construction is expected to increase slightly in 2010 as consumers make improvements rather than moving up, and the age of the housing stock requires improvements.

“The nonresidential sector will see another year of double-digit decline in 2010. Health care, educational and transportation are the only segments that will remain near flat. These segments are less dependent on the general economy. Public safety construction will be the only segment likely to see actual growth. This growth is driven mainly by military construction. The lodging, office and commercial segments are highly cyclical and will experience severe declines in 2010. Manufacturing construction, which has remained strong mostly due to refinery work, will turn down as many of these mega projects are completed.

“The economy may show some signs of improving, but it is just the beginning of the downfall for nonresidential construction. Nonresidential construction typically lags the general economy by about 18 months. Intense competition that has been bringing down prices has been reported. This is good for owners, but not so good for contractors. Nonbuilding construction will remain positive for the forecast period with power and conservation and development leading the sector.”

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!

.webp?height=740&t=1767036885&width=auto "Header - BE 1170x658 (002).png")

.webp?height=740&t=1755781744&width=auto "KEE(2).png")